Small business Group health insurance is employer-sponsored medical coverage available to companies with 2 to 50 full-time employees in Texas. It allows you to offer your team health benefits through a shared plan – often at lower per-person rates than individual coverage – while your business may qualify for tax deductions. This guide walks you through every plan type available in Texas, what each typically costs, who qualifies, and how to get started.

Small businesses group health insurance in Texas is a single policy that covers multiple employees. Your business selects a carrier and plan tier. Employees enroll during an open enrollment window. The employer typically pays a portion of the monthly premium, and employees cover the rest through payroll deductions. In Texas, small-group plans must cover the 10 essential health benefits required by the ACA.

What Is Group Health Insurance for Small Business?

Group health insurance for small business is a single health plan purchased by an employer that provides medical coverage to eligible employees and, in many cases, their dependents. Rather than each person buying an individual policy, the entire team shares a single plan at negotiated rates.

Here is how health insurance group plans for small businesses generally work:

- The employer selects a plan (or a menu of plans) from a carrier like Cigna, UHC, BCBS, Humana, or Aetna.

- Employees enroll during an open enrollment period or within 30 days of becoming eligible.

- Premiums are split between the employer and employees. Texas does not require a specific employer contribution percentage, but most carriers require the employer to cover at least 50% of the employee-only premium.

- Claims are pooled, meaning the risk is spread across the group rather than priced individually.

The main advantage is cost. Group rates are typically lower than individual market rates because the insurance carrier spreads risk across multiple people. Employees also benefit from pre-tax premium payments through payroll deduction.

Group plans in Texas must comply with the Affordable Care Act (ACA). This means they cover ten essential health benefits, cannot deny coverage for preexisting conditions, and cannot charge more based on health status.

Specific plan features, premiums, and coverage details vary by carrier and plan selected.

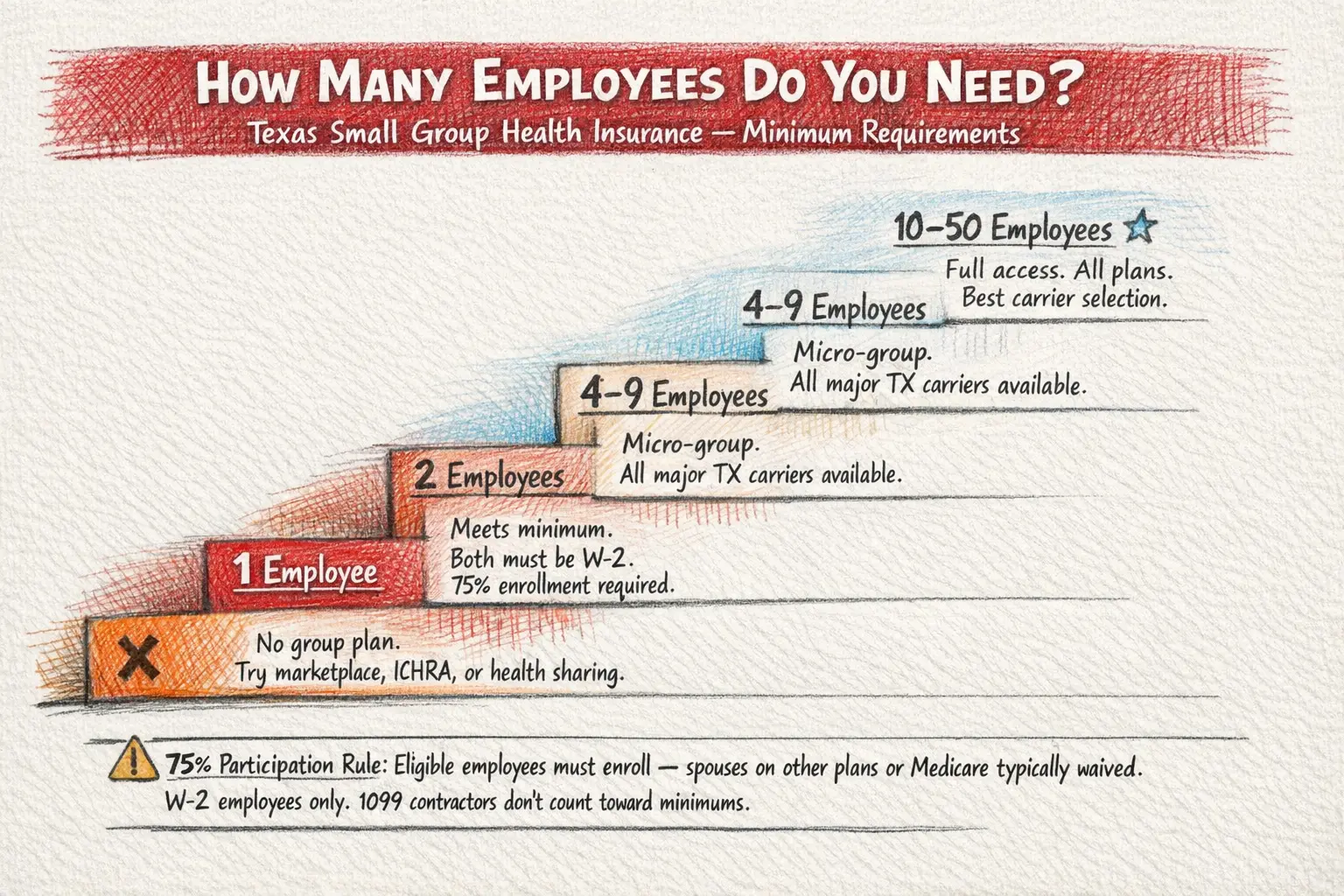

What Is the Minimum Number of Employees for Group Health Insurance in Texas?

In Texas, you generally need at least 2 full-time employees to qualify for a small group health insurance plan. The Texas Department of Insurance defines a “small employer” as a business with 2 to 50 eligible employees.

Here is how the employee count breaks down:

- 1 employee (sole proprietor, no W-2 staff): You typically do not qualify for group health insurance in Texas. You would need to explore individual marketplace plans, an ICHRA, or a health sharing program.

- Health insurance for a small business with 2 employees: You meet the minimum threshold. Both employees must be W-2 workers (not 1099 contractors). Most carriers require at least 75% of eligible employees to enroll.

- Health insurance for small business with 3 employees: You qualify and may have slightly more carrier options, since some carriers prefer groups of 3 or more

- Health insurance for small business with less than 10 employees: You are in the “micro-group” category. All major Texas carriers offer plans for this size, though plan selection may be more limited than for larger groups.

- 10-50 employees: Full access to all small group plans and carrier options

Participation requirements matter. Most Texas carriers require 75% of eligible employees to enroll in the plan. Employees who already have coverage elsewhere (such as a spouse’s plan or Medicare) are generally waived from this count.

Eligibility rules vary by carrier. A licensed broker can confirm the specific requirements for your situation.

Can an LLC with One Employee Get Group Health Insurance?

An LLC owner who is the only worker in the business generally cannot purchase a traditional group health insurance plan in Texas. Group plans require at least 2 eligible employees, and most carriers do not count an owner as an “employee” unless there is at least one additional W-2 staff member on payroll.

Here is how it typically works for health insurance for LLC owners:

- LLC with 1 owner, 0 W-2 employees: You do not qualify for group coverage. Your options include individual marketplace plans on healthcare.gov, health-sharing programs, or a direct-pay arrangement with a carrier.

- LLC with 1 owner + 1 W-2 employee: You may qualify for group health insurance. The owner can be included as a participant if at least one W-2 employee is also enrolled.

- LLC with 1 owner + spouse on payroll as W-2: Some carriers accept this arrangement, but rules vary. Check with a licensed broker to confirm

More affordable alternatives for solo LLC owners:

- ICHRA (Individual Coverage HRA): If your LLC has at least one W-2 employee, you can reimburse them tax-free for individual health insurance premiums

- QSEHRA: For businesses with fewer than 50 employees that do not offer group coverage, you can reimburse employees up to set annual limits

- Individual marketplace: You may qualify for premium tax credits based on your household income through healthcare.gov

The cheapest health insurance for a small business with one employee often depends on whether you can add a W-2 staff member to meet group plan minimums, or whether an HRA arrangement better fits your budget.

Coverage options and eligibility requirements differ by carrier and plan type. Consult a licensed advisor for your specific situation.

What Are the Best Group Health Insurance Plans for Small Business in Texas?

The best health insurance for small business in Texas depends on your team’s needs, your budget, and which doctors and hospitals your employees prefer.

Five major carriers offer Texas small business health insurance plans with statewide or near-statewide coverage.

Here is a general comparison of group health insurance plans for small business in Texas:

| Carrier | Plan Types Available | Network Size in Texas | Best Known For |

Blue Cross Blue Shield of Texas | HMO, PPO, POS | Largest provider network in Texas | Wide provider acceptance, strong brand recognition |

United Healthone | HMO, PPO, EPO | Extensive statewide network | Nationwide coverage for multi-state businesses |

Cigna | PPO, HMO, HSA-compatible | Growing Texas network | Wellness programs, mental health resources |

Aetna | HMO, PPO, POS | Moderate Texas network (CVS Health integration) | Pharmacy benefits, virtual care options |

Humana | HMO, PPO, HSA-compatible | Moderate Texas network | Preventive care focus, competitive small group rates |

What to consider when choosing the best health insurance plan for a small business:

- Network coverage: Does the plan include the doctors and hospitals your employees use? A PPO offers more flexibility. An HMO is usually less expensive but limits you to in-network providers.

- Plan tier: Bronze plans have the lowest premiums but the highest out-of-pocket costs. Gold plans have higher premiums but lower cost-sharing. Silver is the most common middle ground.

- HSA compatibility: High-deductible plans paired with a Health Savings Account can reduce tax liability for both the employer and employees

- Prescription coverage: Formulary lists and pharmacy networks vary significantly across carriers

The best group health insurance for small businesses isn’t one-size-fits-all. The right carrier depends on your team’s size, preferred providers, and how much your business can contribute toward premiums.

Carrier offerings, networks, and rates change periodically. Confirm current options with a licensed broker or directly with the carrier.

How Much Should a Small Business Pay for Health Insurance?

Small business health insurance costs vary widely based on your location in Texas, the plan tier you select, your employees’ ages, and the employer’s contribution.

There is no single “right” amount, but national and state data provide useful benchmarks.

Average small group health insurance costs:

| Factor | Typical Range |

Average annual premium per employee (single coverage) | Approximately $7,900 to $8,400 |

Average annual premium per employee (family coverage) | Approximately $22,000 to $23,500 |

Average employer contribution (single) | About 80% of the employee-only premium |

Average employer contribution (family) | About 70% of the family premium |

Monthly per-employee cost (employer share, single) | Roughly $450 to $600 depending on plan tier |

What drives group health insurance rates for small business:

- Employee ages: Carriers in Texas can charge up to 3x more for a 64-year-old than for a 21-year-old

- Tobacco use: Premiums can be up to 50% higher for tobacco users

- Plan tier selected: Bronze plans cost less monthly but have higher deductibles. Gold plans cost more monthly but cover more at the point of care.

- Location: Premiums vary by Texas rating area. Dallas-Fort Worth, Houston, and Austin each have different rate structures

- Group size: Larger groups generally get more competitive rates

Using a small business health insurance cost calculator: Many carriers and broker websites offer online tools where you enter your ZIP code, number of employees, and age range to get preliminary estimates. These calculators provide ballpark figures, not binding quotes.

If you are wondering how much group health insurance costs for a small business, the most accurate answer comes from requesting formal quotes through a licensed broker who can compare rates across all five major Texas carriers.

All cost figures shown are approximate averages. Your actual premiums depend on your specific group demographics, plan selection, and carrier. Consult a licensed broker for accurate quotes.

What Is the SHOP Marketplace and Why Do Most Texas Businesses Skip It?

The SHOP (Small Business Health Options Program) Marketplace is a government-run platform where small businesses can technically shop for health insurance online. You may have come across it while researching group coverage. Here is what you need to know before deciding how to shop for health insurance for small business.

The one reason SHOP exists: The Small Business Health Care Tax Credit is only available to employers who purchase coverage through SHOP. Businesses with fewer than 25 FTE employees, paying average annual wages below approximately $56,000, may qualify for a credit covering up to 50% of employer-paid premiums.

That tax credit is significant – but for most Texas small businesses, it is the only advantage SHOP offers. Here is why most business owners work with a local broker instead.

Why the SHOP marketplace falls short for most small businesses:

- Fewer carrier options: In many Texas counties, SHOP only has one or two participating carriers. A local broker can access all five major carriers (Cigna, Humana, UHO, BCBS of Texas, Aetna) plus regional options.

- Limited plan types: SHOP may not offer HSA-compatible high-deductible plans, which are one of the most popular cost-saving options for small businesses

- No personalized guidance: You are browsing plans on a website with no one to explain the differences, answer questions about your team’s specific needs, or help with claims issues down the road

- Same prices, less support: Carrier premiums are the same whether you buy through SHOP, direct from a carrier, or through a broker. The plan costs you nothing extra through a broker – carriers pay the broker’s commission.

- No ongoing support: When an employee has a billing dispute or a claim is denied, SHOP does not help. A local broker picks up the phone and advocates for your team.

What a local health insurance broker does that SHOP cannot:

- Compares every available plan across all major Texas carriers in a single side-by-side presentation tailored to your team’s demographics

- Identifies the tax credit and helps you determine if SHOP enrollment makes sense, specifically for the credit, while also showing you off-marketplace plans that may save more overall

- Handles enrollment paperwork, carrier communication, and employee questions so you can focus on running your business

- Provides year-round support for claims issues, employee changes, new hire enrollments, and annual renewals

- Costs you nothing extra – broker commissions are built into carrier pricing, whether you use a broker or not

If you do qualify for the SHOP tax credit, a licensed broker can help you enroll through the SHOP health insurance marketplace to claim it – while also advising whether the credit outweighs the limitations.

In many cases, the broader plan selection and hands-on support from a broker deliver more value than the credit alone.

The bottom line: when you shop for insurance for a small business, working with a local Texas broker gives you more choices, better support, and the same pricing – with someone in your corner when things get complicated.

Tax credit eligibility and SHOP participation vary. A licensed broker can review your situation and determine the best path for your business.

Can Small Businesses Group Together for Health Insurance?

Yes, small businesses can sometimes group together for health insurance through certain arrangements, though the options have specific rules and limitations. Small business health insurance pools and similar structures allow multiple small employers to combine their employees into one larger risk pool, which may result in more competitive rates.

Ways small businesses can pool resources for group health insurance:

- Association Health Plans (AHPs): Small businesses in the same industry or geographic area can join a trade or professional association that sponsors a health plan. For example, a local chamber of commerce or industry group may offer an AHP. These plans are regulated by the Department of Labor and must follow ACA rules for large groups if they cover enough members.

- Professional Employer Organizations (PEOs): A PEO acts as a co-employer, pooling your staff with employees from other small businesses. This larger group can often access better rates and more plan options. The PEO handles HR, payroll, and benefits administration.

- Multiple Employer Welfare Arrangements (MEWAs): Formal arrangements in which multiple employers contribute to a shared fund for health benefits. MEWAs are regulated at both the state and federal levels and must register with the Texas Department of Insurance.

- Health insurance purchasing cooperatives: Some states allow small businesses to form cooperatives for the specific purpose of buying group health insurance together

Important considerations:

- Not all pooling arrangements offer the same protections as standard small group plans.

- ACA consumer protections (like guaranteed issue and essential health benefits) may apply differently depending on the structure

- Costs, plan options, and administrative requirements vary by arrangement.

For group health insurance for small business owners exploring pooling, the key is to verify that the arrangement is properly licensed and regulated in Texas.

Pooling arrangements involve complex regulatory requirements. Consult a licensed benefits advisor or attorney before joining one.

What Is the Most Widely Accepted Health Insurance in Texas?

Blue Cross Blue Shield of Texas (BCBSTX) generally has the largest provider network in the state, making it one of the most widely accepted health insurance options for Texas small businesses.

However, “most widely accepted” depends on the specific plan type (HMO vs. PPO) and your employees’ locations.

How major carriers compare for network coverage in Texas:

| Carrier | Network Reach | Notes |

BCBS of Texas | Largest statewide network | PPO plans accepted by the most Texas providers |

United Healthone | Extensive statewide | Strong in metro areas (DFW, Houston, Austin, San Antonio) |

Cigna | Growing network | Open Access Plus PPO offers broad out-of-network coverage |

Aetna | Moderate | Stronger in major metros, more limited in rural areas |

Humana | Moderate | Solid in DFW and Houston, thinner in West Texas |

What “widely accepted” means for your business:

- If your employees are spread across Texas, a PPO from BCBSTX or UHC typically offers the most flexibility.

- If your team is concentrated in one metro area like Dallas-Fort Worth, most carriers will have strong local networks.

- HMO plans are less expensive but restrict employees to a specific network. PPO plans cost more but allow out-of-network visits at a higher cost-share

For the best health insurance for small business owners, network size is just one factor. You also need to weigh premium costs, plan benefits, and employee preferences.

Network sizes and provider participation change regularly. Verify that your employees’ preferred doctors are in-network before selecting a plan.

How Do You Compare Group Health Insurance Quotes for Small Business?

Comparing group health insurance quotes for small businesses means looking beyond the monthly premium. The cheapest plan may cost you more in the long run if employees face high deductibles and out-of-pocket expenses that reduce the plan’s perceived value.

What to compare across group health insurance plans for small business:

- Monthly premium per employee: This is the sticker price, but it is not the full picture. Compare what the employer pays and what employees pay

- Deductible: The amount employees pay before insurance kicks in. Individual deductibles for small group plans typically range from $500 (Gold) to $7,000+ (Bronze)

- Copays and coinsurance: What employees pay at the doctor’s office, pharmacy, or hospital after meeting the deductible

- Out-of-pocket maximum: The most an employee will pay in a year. Once reached, the plan covers 100% of eligible expenses.

- Network adequacy: Are your employees’ current doctors and hospitals in-network? This is often the single biggest factor in employee satisfaction.

- Prescription drug coverage: Check the formulary. Does it cover the medications your employees currently take? At what tier?

- Additional benefits: Some plans include vision, dental, mental health, telehealth, or wellness programs at no extra cost

How to get the best health insurance plan for a small business:

- Request quotes from at least 3 carriers to see the full range of pricing and options.

- Work with a licensed broker who can access all major carriers simultaneously. Brokers are typically paid by the carrier, so there is no added cost to you.

- Compare plans at the same metal tier (Bronze to Bronze, Silver to Silver) for an apples-to-apples view.

- Factor in the total cost of care, not just the premium. A low-premium, high-deductible plan may cost employees more overall.

When you request group health insurance quotes for a small business, a broker will typically need your business ZIP code, number of employees, employee ages, and desired contribution level.

Quotes are estimates based on census data. Final rates may differ after underwriting. Always confirm details with the carrier or your broker.

What Tax Benefits Do Small Businesses Get for Offering Health Insurance?

Small businesses that offer group health insurance may qualify for several tax advantages. These can significantly reduce the effective cost of providing coverage, making health insurance for small business owners more affordable than the sticker price suggests.

Key tax benefits for group health insurance for small business owners:

Small Business Health Care Tax Credit (SHOP only)

- Available to businesses with fewer than 25 FTE employees

- Average annual wages must be below approximately $56,000 (adjusted annually for inflation)

- You must pay at least 50% of employee-only premium costs.

- The maximum credit is 50% of employer-paid premiums (35% for tax-exempt organizations)

- You must purchase coverage through the SHOP Marketplace to qualify.

Employer premium contributions are tax-deductible.

- The portion of premiums your business pays is generally deductible as a business expense.

- This applies to all group health insurance, not just SHOP plans.

- The deduction reduces your taxable business income.

Section 125 (Cafeteria) Plan

- Allows employees to pay their share of premiums with pre-tax dollars

- Reduces payroll taxes (FICA) for both the employer and employee

- The employer may save approximately 7.65% on every dollar employees contribute pre-tax.

Self-employed health insurance deduction

- If you are a sole proprietor, LLC member, or S-corp shareholder with W-2 wages, you may deduct health insurance premiums on your personal tax return.

- This is an above-the-line deduction, meaning you get it whether or not you itemize

Important: Tax rules are complex and change periodically. The credits and deductions described above are general overviews. Consult a qualified tax professional or CPA to determine what your business qualifies for.

This section is for educational purposes only and does not constitute tax advice.

How Do I Get Group Health Insurance for My Small Business in Texas?

Getting group health insurance for a small business in Texas is straightforward, but it involves several steps. Planning ahead – especially around enrollment timing – helps ensure a smooth rollout.

Step-by-step process to get group health insurance for your small business:

Determine your budget and contribution level.

- Decide how much your business can contribute toward employee premiums each month.

- Most Texas carriers require the employer to cover at least 50% of the employee-only premium.

Gather your employee census data.

- You will need: full names, dates of birth, ZIP codes, employment status (full-time vs. part-time), and whether each employee wants coverage.

- This data is required for carriers to generate accurate group health insurance quotes.

Contact a licensed broker or go direct.

- A broker compares group health insurance plans for small businesses across multiple carriers at no cost to you.

- In Texas, major carriers include Cigna, Humana, UHO, BCBS of Texas, and Aetna.

Review and compare quotes.

- Compare at least 3 options side-by-side.

- Look at premiums, deductibles, networks, and total cost of care (see the comparison section above)

Select a plan and complete the application.

- Your broker or carrier representative will guide you through the application.

- Provide business documentation: EIN, proof of business, and employee roster.

Hold an employee enrollment period.

- Employees have a set window (usually 30 days) to enroll or waive coverage.

- Remember the 75% participation requirement most carriers enforce

Set up payroll deductions.

- Configure your payroll system to deduct employee premium contributions.

- Consider setting up a Section 125 plan for pre-tax premium payments.

Coverage begins

- Most group plans have a first-of-the-month effective date.

- Plans typically renew annually, with rate adjustments at each renewal.

Timing tip: Start the process at least 30 to 60 days before your desired coverage start date. If you want January coverage, begin gathering quotes in October or November.

For group health insurance for small businesses in Texas, Custom Health Plans has helped businesses across the Dallas-Fort Worth area and throughout Texas find the right coverage for over 30 years.

Enrollment processes and requirements vary by carrier. A licensed broker can walk you through each step.

What Are the Alternatives If Your Business Does Not Qualify for Group Coverage?

If your business has fewer than 2 employees, or if traditional group health insurance is outside your budget, several alternatives can still provide health coverage for your team.

Options for businesses that do not meet group plan requirements:

ICHRA (Individual Coverage Health Reimbursement Arrangement)

- Your business sets a monthly allowance. Employees purchase their own individual health insurance and get reimbursed tax-free up to the allowance amount.

- No minimum or maximum group size

- You control the budget. Employees choose their own plan.

- Popular option for health insurance for a small business with one employee (plus an owner)

QSEHRA (Qualified Small Employer HRA)

- For businesses with fewer than 50 employees that do not offer group health insurance

- Maximum reimbursement limits are set by the IRS annually (approximately $6,150 for self-only and $12,450 for family in 2025)

- Employees must have minimum essential coverage to receive reimbursements.

Individual marketplace plans (healthcare.gov)

- Employees purchase their own plans on the ACA marketplace.

- They may qualify for premium tax credits based on household income.

- No employer involvement required, though you can inform employees about this option

Health sharing programs

- Not insurance, but a cost-sharing arrangement among members with similar beliefs

- Monthly costs are often lower than traditional premiums.

- Not regulated like insurance. Payments are not guaranteed, and preexisting conditions may be excluded.

Direct Primary Care (DPC) + catastrophic coverage

- Employees pay a monthly fee to a DPC physician for unlimited primary care visits.

- Pair with a high-deductible catastrophic plan for major medical expenses

- Can be a cost-effective option for young, healthy teams

For the cheapest health insurance for a small business with one employee, an ICHRA or individual marketplace plan is often the most practical path. These allow flexibility without requiring the group plan minimums.

Each alternative has different tax implications, regulatory requirements, and coverage levels. Discuss your options with a licensed insurance advisor.

Your Next Step: Find the Right Plan for Your Texas Business

Choosing group health insurance for a small business in Texas does not have to be overwhelming. Here is what to remember:

- Texas small-group plans cover businesses with 2 to 50 employees; alternatives exist for smaller teams.

- Five major carriers serve Texas – BCBS, UHC, Cigna, Aetna, and Humana, each of which offers different strengths.

- Average employer costs range from roughly $450 to $600 per employee per month for single coverage, depending on plan tier and location.

- The SHOP Marketplace may unlock tax credits of up to 50% for qualifying businesses.

- A licensed broker compares plans across carriers at no extra cost to you and handles the enrollment process.

Custom Health Plans has helped Texas small businesses find the right health insurance for over 30 years.

Our licensed advisors compare plans from Cigna, Humana, UnitedHealthone, Blue Cross Blue Shield of Texas, and Aetna to find coverage that fits your team and your budget.

Schedule a free consultation:

- Call: (469) 361-4032 or toll-free (877) 749-2241

- Visit: 4601 Old Shepard Place, Suite #104, Plano, TX 75093

- Hours: Monday – Friday, 8 AM – 6 PM | Saturday, 10 AM – 2 PM