UnitedHealthcare is one of the largest sellers of short-term health insurance in the United States, with multiple plan tiers and a presence in Texas. Despite the name, short-term plans can now be locked in for up to 3 years in most states, following the federal enforcement of the 4-month cap’s pause in August 2025.

A licensed Texas broker can compare UHC short-term plans to ACA Bronze and other carriers in a single sitting.

Does UnitedHealthcare sell short-term health insurance in Texas?

UnitedHealthcare and its affiliates have historically sold short-term limited-duration insurance in most U.S. states. State-by-state availability shifts each plan year. A licensed Texas broker can confirm which UHC short-term products are currently writing new business in Texas this quarter.

Three things to know about UHC’s short-term footprint:

- Major national presence: UnitedHealthcare is one of the largest short-term health insurance providers in the country.

- Multiple plan tiers: UHC short-term plans typically come in several deductible and coinsurance tiers, including copay-style and high-deductible options.

- State variations: Availability and plan design vary by state because short-term plans are state-regulated. Texas-specific options should be confirmed at quote time.

A licensed Texas broker can also pull quotes from carriers other than UHC if UHC’s current Texas short-term offering is limited.

Carrier short-term availability changes. Always confirm at the time of purchase.

What does UnitedHealthcare short-term insurance cover?

UHC short-term plans typically cover doctor visits, urgent care, emergency room visits, hospitalization, and some surgical procedures. Many UHC short-term plans include limited prescription drug coverage and add-ons for preventive care.

Maternity and pre-existing conditions are excluded.

Typical UHC short-term coverage elements:

- Doctor visits: Often a copay or coinsurance after deductible.

- Urgent care: Generally covered with a copay.

- Emergency room: Covered after deductible.

- Hospitalization: Covered up to plan benefit caps.

- Prescription drugs: Some plans include limited drug coverage, often with a dollar cap.

- Preventive care: Limited; coverage varies by plan.

What is usually NOT covered:

- Pre-existing conditions: Any condition treated, diagnosed, or symptomatic before the policy starts.

- Maternity: Not covered in short-term plans. Kaiser Family Foundation found 0 of 24 reviewed short-term plans covered maternity.

- Mental health and substance use: Often limited or excluded.

UHC plan terms vary. Read the certificate of coverage before paying any premium.

How much does UnitedHealthcare short-term insurance cost in Texas?

UnitedHealthcare short-term plans in Texas typically cost $80 to $300 per month for a healthy adult, depending on age, deductible, and benefit tier. Premiums are usually 20% to 50% of the cost of an unsubsidized ACA Bronze plan.

Cost drivers:

- Age: A healthy 28-year-old in Houston may pay $90 to $150 per month. A 58-year-old can pay $250 to $400.

- Deductible: Plans with $1,000 deductibles cost more than plans with $7,500 deductibles.

- Coinsurance: Lower coinsurance splits (80/20) cost more than higher splits (50/50).

- Add-ons: such as prescription drug riders and wellness benefits, increase the premium.

For context, COBRA continuation typically costs $400 to $700 per month per individual. ACA Bronze plans in Texas climbed roughly 34.7% gross for 2026 before subsidies.

Quote engine premiums often exclude administrative and rider costs. Verify total cost before enrolling.

How long can you keep UnitedHealthcare short-term insurance in Texas?

Under the current Texas law, short-term plans can last up to 36 months, including renewals. UHC typically offers short-term coverage in 3-, 6-, or 12-month blocks, depending on state availability.

Practical duration options:

- 3 months: A quick bridge for a new job’s waiting period.

- 6 months: Between jobs or after a missed Open Enrollment.

- 12 months: Longer transitions, such as freelance work or a pre-Medicare bridge.

- Up to 36 months total: Allowed under Texas state law via renewals.

Caveat: federal rules from 2024 limited stacking and required a 12-month wait between same-carrier renewals. While enforcement has paused, individual carriers may still apply these rules.

Verify renewal terms with the carrier before assuming a 3-year duration is available.

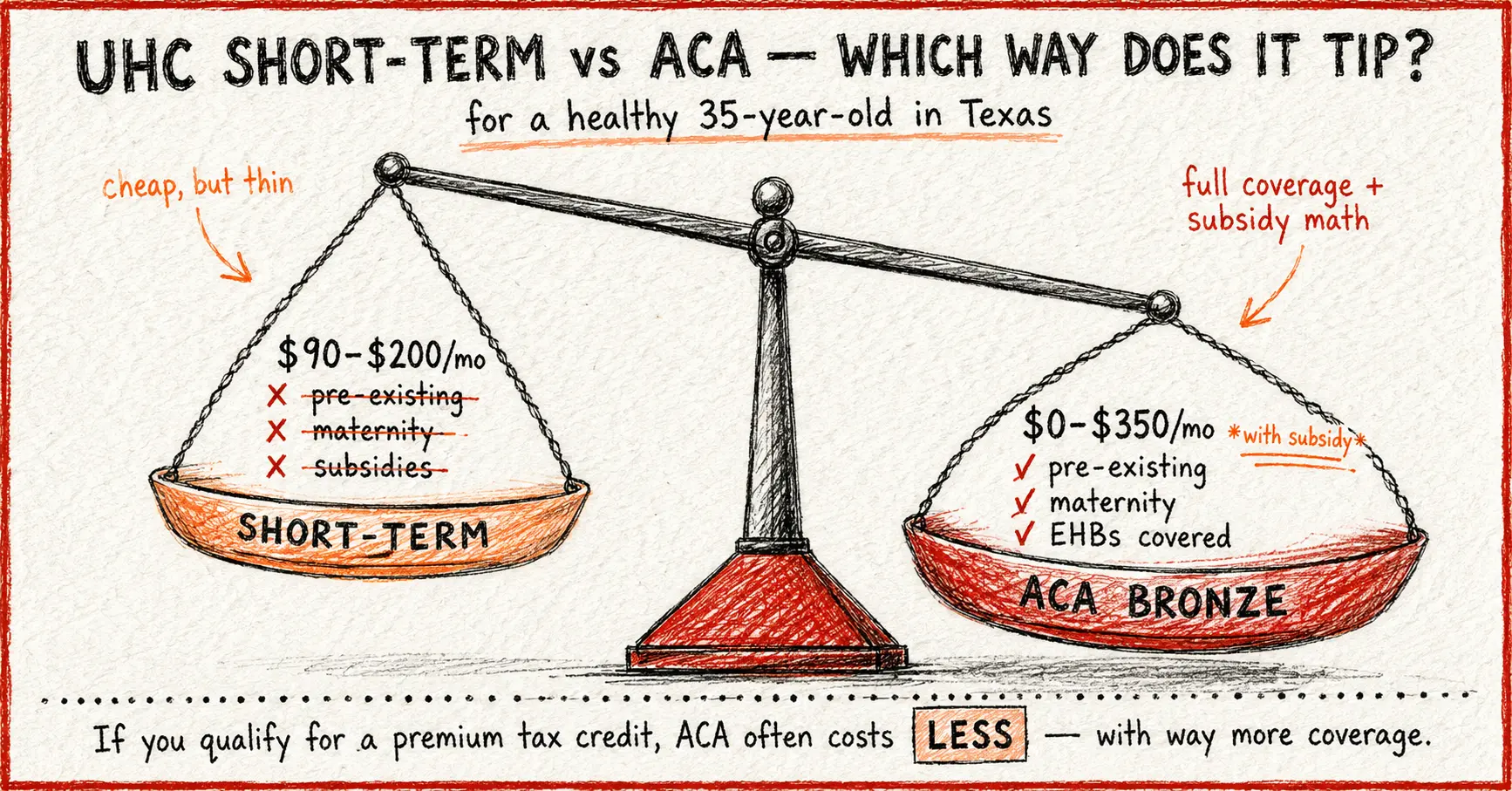

UHC short-term vs UHC ACA plans: which makes sense?

UnitedHealthcare offers both short-term and ACA-compliant plans. ACA plans cost more but cover pre-existing conditions and all essential health benefits. Short-term plans cost less but exclude pre-existing conditions and most ACA essentials.

Quick comparison for a healthy 35-year-old in Texas:

| Plan Type | Typical Monthly | Covers Pre-Existing | Maternity | Subsidies |

| UHC Short-Term | $90 to $200 | No | No | Not eligible |

| UHC ACA Bronze (no subsidy) | $330 to $550 | Yes | Yes | Not used |

| UHC ACA Bronze (with subsidy) | $0 to $350 | Yes | Yes | Yes |

If your household qualifies for an ACA premium tax credit, the ACA plan often becomes cheaper or comparable to short-term coverage with far better benefits.

Subsidy eligibility depends on income and household size. A broker can run the numbers in five minutes.

What are the downsides of UnitedHealthcare short-term insurance?

The biggest downsides are pre-existing condition exclusions, benefit caps, post-claims underwriting risk, and the lack of premium tax credits. UHC short-term plans share these limitations with the rest of the short-term market.

Six trade-offs:

- Pre-existing exclusions: Conditions diagnosed before the policy starts may be denied.

- Benefit caps: Per-surgery, per-day hospital, and per-term prescription caps can leave members exposed.

- Post-claims underwriting: Carriers can review medical history after a claim.

- No subsidies: Tax credits do not apply to short-term coverage.

- No guaranteed renewability: A new condition mid-term may be excluded at renewal.

- Network limits: Some short-term plans use narrow PPO networks.

The Texas Department of Insurance warns that short-term plans “usually offer fewer benefits and have lower coverage amounts than traditional health insurance.”

Anyone with chronic conditions or planned medical needs should be cautious with short-term coverage.

How do you enroll in UnitedHealthcare short-term insurance in Texas?

Enrolling in UHC short-term coverage in Texas takes four steps: identify the gap length, gather basic medical history, get quotes through a licensed broker, and submit the application. Most short-term plans start within 24 to 48 hours.

A practical workflow:

- Define the gap. 30 days, 6 months, 18 months.

- List medications and recent diagnoses.

- Pull quotes from UHC and competing carriers. A broker handles this in one sitting.

- Read the certificate of coverage. Pay attention to pre-existing definitions and benefit caps.

- Apply and confirm the effective date.

Brokers are paid by carriers, not clients. The comparison costs nothing.

Verify carrier complaint history with the Texas Department of Insurance before enrolling.

Is UnitedHealthcare short-term insurance worth it?

UHC short-term insurance is worth it for healthy adults who bridge a finite gap and do not qualify for an ACA subsidy. For chronic conditions, planned pregnancies, or longer-term needs, an ACA plan from UHC or another carrier is usually the better choice.

UHC’s short-term product line is widely available, well-branded, and competitively priced. The same product limitations that affect every short-term plan apply: pre-existing exclusions, benefit caps, and no subsidies.

The question is rarely “is UHC short-term any good,” but rather “is short-term the right tool for my situation?”

This is a personal decision based on health, income, and life circumstances.

Closing thoughts

UnitedHealthcare is a major short-term insurance carrier in the United States with broad national availability.

Texas residents shopping for UHC short-term coverage should also compare UHC short-term coverage with UHC ACA Bronze with potential subsidies, plus options from BCBSTX, Aetna, Cigna, and Humana through a licensed broker.

Three things to do next:

- Write down your exact gap length and basic health profile.

- List anything you cannot afford to lose, such as a specific doctor or pharmacy.

- Schedule a quick call with a licensed Texas broker to compare UHC short-term, UHC ACA, and other carrier options.

A short conversation can clarify the best fit for your situation. Click here for a conversation