Health insurance plans for small business in Texas include group PPO, HMO, HDHP, and EPO plans from carriers like Blue Cross Blue Shield of Texas, Cigna, Aetna, UnitedHealthcare, and Humana.

Texas employers with 2 to 50 employees can also consider ICHRAs or level-funded plans through the private market. Working with a licensed broker gives you access to broader networks, more carriers, and year-round enrollment, plus side-by-side quotes you cannot pull on your own.

The right plan depends on your team size, budget, and whether your employees need PPO flexibility or can work within an HMO network. For a full overview of every option Texas employers have, see our complete 2026 guide to health insurance for small businesses.

What Types of Health Insurance Plans Are Available for Small Businesses in Texas?

Texas small businesses with 2 to 50 employees can choose from six main plan types: group PPO, group HMO, HDHP with HSA, EPO, ICHRA, and level-funded plans. Each balances cost, flexibility, and network access differently.

Here is how each plan type works:

1. PPO (Preferred Provider Organization)

- Largest provider networks, including out-of-state coverage

- No referral needed to see a specialist

- Higher monthly premiums, but greater flexibility

- Available from Blue Cross Blue Shield of Texas, Cigna, Aetna, UnitedHealthcare, and Humana

2. HMO (Health Maintenance Organization)

- Lower premiums than PPO

- Requires a primary care physician (PCP)

- Referral required for specialists

- Limited to in-network providers only (except emergencies)

For a deeper side-by-side breakdown of these two networks, read our HMO vs PPO comparison.

3. HDHP (High-Deductible Health Plan) with HSA

- Lowest monthly premiums of any group plan type

- Higher deductibles ($1,650+ for individual, $3,300+ for family in 2025)

- Pairs with a Health Savings Account (HSA) for tax-advantaged medical savings

- Employees can roll over unused HSA funds year to year

If you are new to HSAs, this beginner’s guide to Health Savings Accounts walks through the tax benefits and rules.

4. EPO (Exclusive Provider Organization)

- No out-of-network coverage except emergencies

- No referral requirements for specialists

- Lower premiums than PPO, higher than HMO

5. ICHRA (Individual Coverage Health Reimbursement Arrangement)

- You set a fixed monthly allowance per employee

- Employees purchase their own individual plans through a broker on the private market

- No participation minimum required

- You control costs; employees choose their own coverage

- Available since 2020 under IRS rules

6. Level-Funded Plans

- A hybrid between fully insured and self-funded

- You pay a fixed monthly amount; if claims come in lower than expected, you may receive a refund

- Typically available for groups of 5-10+ employees, depending on the carrier

- Offered by carriers like UnitedHealthcare and Cigna in Texas

Plan availability varies by county, carrier, and group size. Not all plan types are available in every Texas market.

If you have just one employee (or it is just you and a spouse), see our guide to small business health insurance for one employee.

What Is the Best Health Insurance Plan for a Small Business?

There is no single best health insurance plan for every small business. The right choice depends on your budget, your team’s demographics, and the level of flexibility your team needs. For a full breakdown of how to evaluate fit, read best health insurance coverage for small business owners.

Decision framework by priority:

- If your priority is the widest provider access, consider a PPO. Nationwide networks, no referrals, and out-of-state coverage.

- If your priority is the lowest monthly premiums, consider an HMO or HDHP. Lower cost, but limited networks (HMO) or higher deductibles (HDHP).

- If your priority is employee choice, consider an ICHRA. Employees pick their own plans; you set the budget.

- If your priority is cost predictability with upside, consider a Level-Funded plan. Fixed monthly cost with a potential refund if claims are low.

- If your priority is travel coverage, consider a PPO or EPO. In-network coverage beyond your home metro area.

- If your priority is the lowest total cost across carriers, consider a broker-accessed group plan. Quotes from 5+ carriers in one place, no DIY guesswork.

According to the KFF 2025 Employer Health Benefits Survey, 76% of smaller businesses choose a single plan for all employees. If you can only offer one plan, a PPO provides the most flexibility, while an HMO keeps costs lower.

The best plan for your business depends on your group’s age mix, location, and health needs. A licensed broker can model the cost of each option for your specific team without you ever logging into a public exchange or sorting through plans on your own.

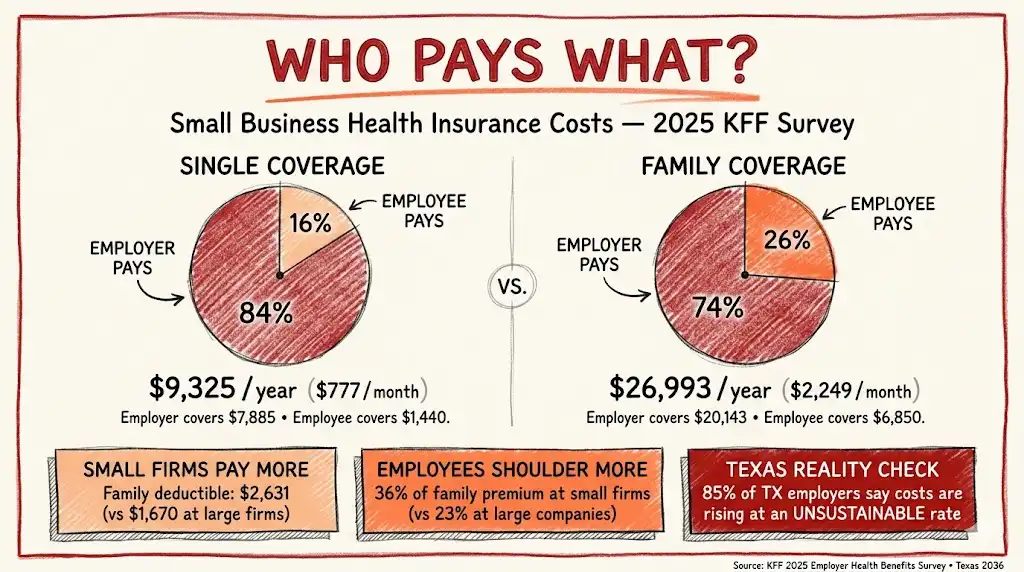

How Much Do Health Insurance Plans Cost for a Small Business?

The national average annual premium for employer-sponsored health insurance in 2025 is $9,325 for single coverage and $26,993 for family coverage, according to the KFF 2025 Employer Health Benefits Survey.

Family premiums increased 6% in 2025 and have risen 26% since 2020. For Texas-specific numbers and a county-level view, see our breakdown of how much small business health insurance costs in Texas.

Cost breakdown by who pays what:

- Single coverage – Annual premium: $9,325 ($777/mo). Employer pays $7,885 (84%). Employee pays $1,440 (16%).

- Family coverage – Annual premium: $26,993 ($2,249/mo). Employer pays $20,143 (74%). Employee pays $6,850 (26%).

Small business-specific figures:

- Small firms (10-199 workers) have average family deductibles of $2,631 vs $1,670 at larger firms

- Small business employees contribute 36% of family premiums compared to 23% at large companies

- Aon projects employer health insurance costs will exceed $17,000 per employee in 2026, a 9.5% increase

Texas context: A 2024 survey by Texas 2036 found 85% of Texas employers say healthcare costs are rising at an unsustainable rate, and 51% say those costs limit their ability to raise wages or hire.

If budget is the bottleneck, our guide to affordable health insurance for small business lays out the levers most owners overlook.

Your actual premiums depend on employee ages, your Texas county, plan design, and carrier. A broker can run quotes across multiple carriers to find the most cost-effective plan for your specific group.

These are national averages from the KFF 2025 survey. Your premiums will vary based on your group’s demographics and location.

Why Buying Through a Broker Beats Buying on Your Own

Texas small employers technically have a few ways to shop for coverage, but the differences in network access, carrier choice, and ongoing service are significant.

Working with a licensed Texas broker gives you the widest plan selection, real PPO networks, and a single point of contact for renewals and claims issues.

There is no extra cost for using a broker; carriers build the same commission into the premium whether you go direct or use a broker.

Broker-accessed plans vs DIY / self-serve options:

- Plan types – Through a broker: PPO, HMO, HDHP, EPO, level-funded, and ICHRA. DIY: limited HMO-style options.

- Carriers available – through a broker: 5+ (BCBS TX, Cigna, Aetna,

UnitedHealthcare, Humana, Texicare). DIY: narrow selection. - Enrollment timing – Through a broker: year-round. DIY: often tied to a fixed window.

- Network scope – Through a broker: PPO plans offer nationwide coverage. DIY: local HMO networks only.

- Specialist referral – Through a broker: not required (PPO/EPO). DIY: required (HMO).

- Broker guidance – Through a broker: full comparison and ongoing support. DIY: you are on your own.

- Coverage start – Through a broker: as fast as 1-15 days. DIY: tied to enrollment dates.

What this means in practice: a broker pulls live quotes across every carrier appointed in your county, models PPO vs HMO vs ICHRA against your team’s age mix, and handles enrollment paperwork, COBRA notices, and renewal shopping for you every year.

Trying to compare plans on your own usually means narrower networks, fewer carriers, and no one to call when a claim is denied. For a full breakdown of what a good broker should do for you, see why work with a health insurance broker for small business.

Plan availability, network sizes, and premiums vary by county. A licensed Texas broker can tell you exactly which carriers are competing for your business this year.

Is It Cheaper to Get Health Insurance Through an LLC?

Forming an LLC does not automatically lower your health insurance premiums. However, it can change which plan types you access and may create tax advantages.

How an LLC affects your options:

- Single-member LLC with no W-2 employees – you typically cannot purchase group health insurance. You would buy an individual plan through a broker on the private market.

- LLC with 2+ W-2 employees – you qualify for group plans in Texas, which can offer lower per-person rates than individual plans due to risk pooling.

- S-Corp election – if your LLC elects S-Corp tax status, you can deduct 100% of health insurance premiums as a business expense (above-the-line deduction).

According to the PeopleKeep Texas guide, individual premiums can actually be lower than small group rates in some Texas counties, by $10-15/month for a comparable silver plan.

This means buying individual coverage through a broker-supported ICHRA may cost less than a traditional group plan, while still providing a structured employer benefit.

If you are a solo founder or self-employed, our guide to group health insurance for self-employed Texans walks through the entity-by-entity rules.

The cost advantage depends on your entity structure and number of employees.

Tax treatment of health insurance premiums varies by entity type. Consult a CPA or tax advisor for your specific situation, and let a broker handle the plan comparison.

What Are the Requirements for Small Business Health Insurance in Texas?

The Texas Department of Insurance (TDI) sets the rules for small group health coverage in Texas.

The Affordable Care Act (ACA) does not require employers with fewer than 50 full-time equivalent employees to offer health insurance, but if you choose to offer it, specific rules apply.

For the full eligibility and enrollment checklist, see small business health insurance requirements.

Texas small group requirements:

- Employer size – 2 to 50 employees qualifies as a small employer under Texas law

- Employee eligibility – must offer coverage to all employees working 30+ hours per week

- Dependent coverage – must include the option for dependent enrollment

- Participation threshold – most carriers require at least 75% of eligible full-time employees to enroll. Workers with coverage from another source (spouse’s plan, Medicare, VA) don’t count against this threshold

- Guaranteed issue – carriers cannot deny coverage or exclude preexisting conditions

- Age rating cap – a 64-year-old’s premium cannot exceed 3 times the rate for a 21-year-old on the same plan

- Waiting period – coverage may be delayed up to 90 days after enrollment (no premiums during wait)

- New hire enrollment – new employees must receive at least 31 days from the start date to enroll

Employer contribution: While Texas does not mandate a minimum employer contribution, most carriers require that the employer pay at least 50% of the employee-only premium to maintain the group plan.

Regulations can change. Verify current requirements with TDI or a licensed broker before making enrollment decisions.

Why Are Fewer Small Businesses Offering Group Health Insurance?

Only 54% of firms with 10-49 employees offered health benefits in 2025, down from 78% in 1999, according to KFF. In Texas specifically, roughly 62% of small businesses do not offer coverage.

The top reasons small businesses drop or skip group coverage:

- Rising premiums – family coverage premiums have risen 26% since 2020. In Texas, 85% of employers say costs are unsustainable

- Participation minimums – the 75% enrollment threshold is hard to meet when younger employees opt out

- Administrative burden – managing enrollment, compliance, and renewals takes time; small teams don’t have

- Avoidable mistakes – many owners pick the wrong plan type, miss carrier discounts, or overpay because they shop without a broker. See 5 mistakes costing small businesses thousands on employee health insurance

What this means for you: If traditional group insurance feels out of reach, an ICHRA lets you offer a defined contribution toward individual coverage. You set the budget. Employees choose their own plans (with broker guidance).

There is no participation minimum. This has made ICHRAs the fastest-growing alternative for businesses with under 50 employees.

That said, group plans still offer advantages: risk pooling lowers per-person costs for older teams, and employees value the simplicity of employer-selected coverage. Our group health insurance for small business guide compares both side-by-side.

Coverage decisions should take into account your team’s demographics, budget, and preferences. A broker can model both group and ICHRA options for you in one conversation.

Which Carriers Offer Small Business Health Insurance in Texas?

Texas small businesses can access plans from both national and regional carriers. The available carriers vary by county and plan type.

Major carriers for Texas small group plans:

- Blue Cross Blue Shield of Texas – Plan types: PPO, HMO, HDHP. Network scope: statewide (largest TX network). Notable feature: broadest provider directory.

- UnitedHealthcare – Plan types: PPO, HMO, HDHP, level-funded. Network scope: national. Notable feature: level-funded options for groups of 2 or more.

- Cigna – Plan types: PPO, HMO, HDHP. Network scope: national. Notable feature: strong behavioral health coverage.

- Aetna – Plan types: PPO, HMO, HDHP. Network scope: national. Notable feature: CVS Health integration for pharmacy.

- Humana – Plan types: PPO, HMO, HDHP. Network scope: regional and national. Notable feature: wellness program incentives.

- Texicare – Plan types: HMO. Network scope: Texas only. Notable feature: designed specifically for TX small businesses.

- Oscar Health – Plan types: HMO. Network scope: select TX counties. Notable feature: digital-first experience with a telemedicine focus.

Key consideration: Not every carrier operates in every Texas county. Rural counties may have as few as 2-3 carrier options, while metro areas like Dallas-Fort Worth, Houston, Austin, and San Antonio typically have 5+ carriers competing for your business.

A broker with appointments at multiple carriers can pull quotes specific to your county and employee group. Custom Health Plans is appointed with all five major Texas carriers (Blue Cross Blue Shield of Texas, Cigna, Aetna, UnitedHealthcare, Humana), so you can compare every real option in one conversation.

Carrier availability changes annually. Verify current options with a licensed broker in your area.

How to Choose the Right Health Insurance Plan for Your Small Business

Selecting a plan requires matching your budget, employee needs, and administrative capacity. Here is a step-by-step process:

- Set your budget – decide the maximum monthly amount you can contribute per employee. The national average employer contribution is $7,885/year for single coverage

- Survey your team – ask employees whether they prioritize lower premiums (HMO/HDHP), provider flexibility (PPO), or individual choice (ICHRA)

- Check your county’s carrier options – not all carriers operate in every Texas county. A broker can identify which carriers serve your area

- Compare plan types – get quotes across PPO, HMO, and HDHP from at least 3 carriers

- Evaluate ICHRA as an alternative – if group plan costs are too high or you can’t meet the 75% participation threshold, an ICHRA may work better

- Get a real quote, not an estimate – generic online estimators don’t reflect your group’s age mix or county. Request a free health insurance quote for small business instead

- Review annually – premiums change every year. A broker who reviews your plan at renewal can catch savings you would miss

Every business is different. A licensed broker can walk you through these steps with actual quotes tailored to your team.

Get a Free Health Insurance Plan Comparison for Your Texas Small Business

Choosing between PPO, HMO, HDHP, and ICHRA plans is easier when you have actual quotes in hand.

A licensed broker compares plans across Blue Cross Blue Shield of Texas, Cigna, Aetna, UnitedHealthcare, and Humana, at no cost to you.

Here is what to do:

- Call Custom Health Plans at (469) 361-4032 for a free, no-obligation plan comparison

- Share your employee count, budget, and whether your team prefers PPO flexibility or HMO savings

- Receive side-by-side quotes from multiple carriers within 24-48 hours

- Get help with enrollment, compliance, and annual renewals

Custom Health Plans has served small businesses across the Dallas-Fort Worth metroplex for over 30 years, including Plano, Frisco, McKinney, Allen, Richardson, and surrounding communities.