Short term health insurance Texas is a privately purchased plan that bridges gaps between major coverage. Despite the name, you can now lock in short-term plans for up to 3 years in most states, including Texas, following the federal government’s August 2025 decision to halt enforcement of the previous 4-month cap.

These plans cost less than ACA-compliant coverage but exclude pre-existing conditions and several essential health benefits.

What is short-term health insurance in Texas?

Short-term health insurance, also called short-term limited-duration insurance (STLDI), is a private medical plan that provides temporary coverage outside the Affordable Care Act framework.

It is medically underwritten, not ACA-compliant, and designed to bridge gaps between major coverage.

Short-term plans in Texas work differently from traditional health insurance in five important ways:

- Medical underwriting: Carriers ask health questions and can decline applicants based on their history.

- Pre-existing exclusions: Any condition treated before the policy starts is generally not covered.

- Limited essential benefits: Plans may skip maternity, mental health, substance use treatment, and prescription drug coverage.

- Faster onboarding: Coverage often begins within 24 hours of payment.

- Lower premiums: Costs are usually a fraction of ACA Bronze plans, especially for healthy applicants.

Major carriers selling short-term coverage in the U.S. include UnitedHealthcare, Cigna (through partner underwriters in select states), Blue Cross Blue Shield, and Allstate (formerly National General). Availability varies by state and renewal year.

Coverage details, premiums, and carrier offerings vary by plan and applicant. Quotes pulled today may not match what’s available next month.

Does Texas allow short-term health insurance?

Direct answer: Yes. Texas allows short-term health insurance. State statute permits an initial term of less than 12 months and a total duration, including renewals, of up to 36 months.

Federal rules briefly capped this at 4 months in 2024, but enforcement was halted on August 7, 2025.

Three regulatory facts every Texas shopper should know:

- The 2024 federal rule from the Departments of Treasury, Health and Human Services, and Labor capped new STLDI plans at a 3-month initial term and 4 months total, effective September 1, 2024.

- On February 19, 2025, President Trump issued an executive order directing agencies to revisit the rule.

- On August 7, 2025, the Departments announced they will not prioritize enforcement of the 4-month cap and encouraged states to follow suit.

For Texas residents, this means short-term plans can be structured for longer than 4 months. The Texas Department of Insurance still references the older 3-month framing on its consumer page, and carrier offerings as of early 2026 vary widely.

A licensed Texas broker can confirm which carriers are currently selling longer-duration short-term plans.

State laws and federal enforcement can shift again. Always confirm current rules at the time of purchase.

How long can you keep short-term health insurance in Texas?

Under the current Texas law, short-term health insurance can last up to 36 months, including renewals. Most carriers currently offer plans in 3-month, 6-month, or 12-month blocks, with renewal options up to the state cap.

This is one of the most misunderstood points in the entire short-term market. Despite the name, “short-term” no longer means a few weeks. Real-world duration options in Texas typically look like this:

- 30 to 89 days: For quick gaps, such as a new job’s waiting period.

- 3 to 6 months: Common bridge between jobs or after a missed Open Enrollment.

- 12 months: Available with some carriers; useful for self-employed Texans waiting on a long-term plan.

- Up to 36 months total: Allowed under Texas state law via consecutive renewals.

There is one important catch. Federal rules introduced in 2024 prohibited “stacking” with the same insurer and required a 12-month wait between policies from the same carrier.

While enforcement has been paused, some carriers still apply these rules voluntarily, and renewing after a major claim may surface pre-existing exclusions on the new policy.

A licensed Texas broker can verify which carriers offer 12-month or longer plans this quarter and walk through the renewal small print.

What does short-term health insurance cover (and not cover) in Texas?

Direct answer: Short-term plans in Texas typically cover doctor visits, urgent care, emergency room visits, hospitalization, and some surgical procedures.

They commonly exclude maternity, mental health, substance use treatment, prescription drugs, and pre-existing conditions.

According to a Kaiser Family Foundation review of short-term plans:

| Benefit | Plans Covering It |

| Mental health services | ~57% |

| Substance use treatment | ~38% |

| Outpatient prescription drugs | ~29% to 52% (varies by carrier) |

| Maternity care | 0 of 24 plans reviewed |

| Preventive care | Limited or none |

| Pre-existing conditions | None |

Even when prescription drug coverage is included, most plans cap it at $3,000 or less per term. Plan documents often hide other limits, such as a per-surgery maximum or a daily hospital reimbursement cap, leaving members with five-figure bills after a major event.

Boundary: Always read the certificate of coverage before paying the first premium. Carriers can lawfully exclude conditions if the application is incomplete or inaccurate.

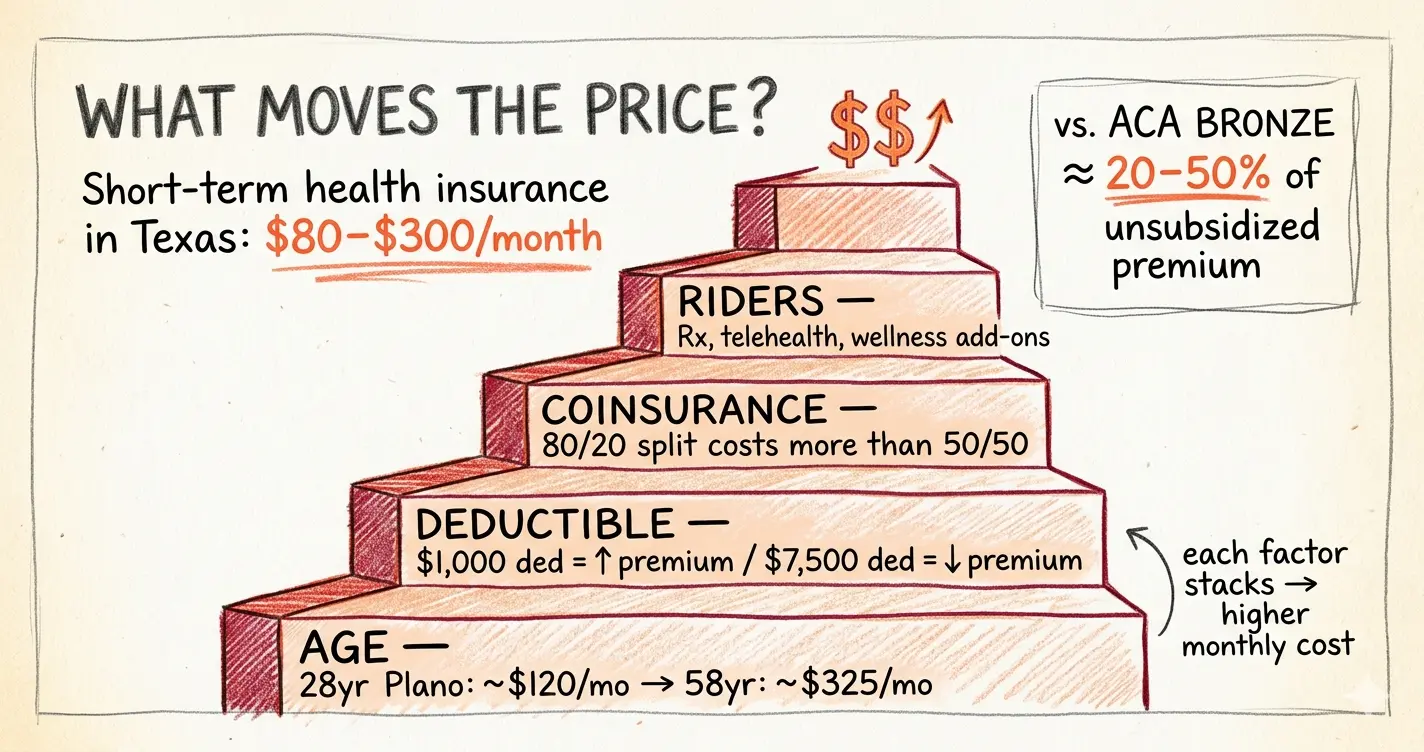

How much does short-term health insurance cost in Texas?

Direct answer: Short-term health insurance in Texas typically costs $80 to $300 per month for a healthy adult, depending on age, deductible, and coverage tier.

That is roughly 20% to 50% of an unsubsidized ACA Bronze premium for the same applicant.

Cost drivers in Texas short-term pricing include:

- Age: A healthy 28-year-old in Plano may pay $90 to $150 per month, while a 58-year-old can pay $250 to $400.

- Deductible: Plans with $1,000 deductibles cost more than plans with $7,500 deductibles.

- Coinsurance split: 80/20 plans cost more than 50/50 plans.

- Optional riders: Prescription drug add-ons, telehealth, and wellness benefits raise the premium.

For context, COBRA continuation typically costs $400 to $700 per month per individual (about $13,000 per year), and unsubsidized ACA Bronze premiums in Texas climbed significantly for 2026, with statewide rate filings averaging roughly +34.7% gross over the prior year.

About 92% of Texas Marketplace enrollees qualify for premium tax credits, so the right comparison depends on whether the applicant qualifies for subsidies through a broker-guided enrollment.

Premiums shown by quote engines often exclude administrative fees and rider costs. A licensed Texas broker can run an apples-to-apples comparison across short-term, ACA, COBRA, and employer plans.

What are the downsides of short-term health insurance?

The biggest downsides of short-term health insurance are pre-existing condition exclusions, limited essential benefits, post-claims underwriting risk, and the lack of premium tax credits.

These plans can leave members exposed to large bills after a serious illness or injury.

Six trade-offs to weigh before buying:

- Pre-existing exclusions: Any condition treated, diagnosed, or symptomatic before the policy starts can be denied.

- Post-claims underwriting: Carriers can review medical history after a claim and rescind coverage if the application is found inaccurate.

- Benefit caps: Many plans cap surgical, hospital, and prescription benefits at amounts well below actual cost.

- No subsidies: Premium tax credits and cost-sharing reductions do not apply.

- No guaranteed renewability: If you develop a new condition mid-term, renewal may exclude that condition.

- Network limits: Some plans use limited PPO networks; out-of-network bills may not be covered.

The Texas Department of Insurance warns specifically about post-claims underwriting and renewal risk: “When a plan ends, you have to buy a new plan. If you’re sick, you might not be able to get another short-term plan.”

These trade-offs make short-term coverage a poor fit for anyone with ongoing health needs, family planning, or chronic conditions.

Who should consider short-term health insurance in Texas?

Short-term plans fit healthy adults, bridging a coverage gap of 30 days to 3 years.

They work best for between-jobs transitions, new-employer waiting periods, missed Open Enrollment, early retirement before Medicare, and young adults aging off a parent’s plan at 26.

Five Texas-specific use cases:

- Between jobs: A laid-off Dallas software engineer covering 90 days before a new role’s benefits begin.

- New-job waiting period: A Plano nurse with a 60-day waiting period at a new hospital.

- Missed Open Enrollment: A Fort Worth resident who missed the December 15 deadline and has no qualifying life event.

- Early retirement bridge: A 60-year-old Plano retiree bridging coverage until Medicare at 65.

- Self-employed transition: A freelancer in Houston waiting on an ACA Special Enrollment Period.

Short-term coverage is not a fit for anyone with ongoing prescription needs, a planned pregnancy, an active chronic condition, or a need for guaranteed long-term coverage.

A licensed broker can run side-by-side comparisons against COBRA, ACA Bronze, and employer plans before any application is signed.

Short-term vs ACA vs COBRA: which is right for a Texas resident?

Short-term insurance fits healthy adults in a temporary gap. ACA Bronze with a premium tax credit usually wins for households earning under 400% of the federal poverty level.

COBRA fits people who need to keep an existing doctor or pharmacy network during a transition.

Quick comparison for a healthy 35-year-old non-smoker in the Dallas-Fort Worth metro:

| Option | Typical Monthly Cost | Pre-Existing | Prescription Drug | Best For |

| Short-Term (STLDI) | $90 to $200 | Not covered | Limited or capped | Healthy bridge coverage |

| ACA Bronze (no subsidy) | $330 to $550 | Covered | Covered | Higher income, planned care |

| ACA Bronze (with subsidy) | $0 to $350 | Covered | Covered | Lower to mid income, full benefits |

| COBRA | $400 to $700 | Covered | Covered | Continuity of doctors and pharmacy |

Most healthy single adults under 50 in Texas find ACA with a subsidy or short-term coverage cheaper than COBRA. Anyone with a pre-existing condition usually leans toward the ACA or COBRA over short-term plans.

The right answer depends on the applicant’s income, health, family size, and the duration of the coverage gap.

How do you buy short-term health insurance in Texas?

Buying short-term health insurance in Texas takes four steps: identify the gap length, gather basic medical history, compare carrier quotes through a licensed broker, and submit the application. Coverage typically starts within 24 to 48 hours.

A practical workflow:

- Define the gap. How many months of coverage do you actually need?

- Map your health profile. List medications, recent diagnoses, and any planned procedures.

- Compare quotes from multiple carriers. Premiums, deductibles, and exclusions vary widely between Blue Cross Blue Shield of Texas, UnitedHealthcare, Aetna, Cigna, and others.

- Read the certificate of coverage. Especially the pre-existing condition definition and any benefit caps.

- Apply and confirm the effective date. Most carriers begin coverage the day after payment clears.

Working with a licensed Texas broker like Custom Health Plans simplifies the comparison process because the broker can pull quotes from multiple carriers, explain the fine print clearly, and check whether an ACA Special Enrollment Period or another option would actually serve you better.

Brokers are paid by carriers, not by clients, so the comparison costs nothing out of pocket.

Always verify the carrier’s complaint history with the Texas Department of Insurance and read the policy certificate before paying.

Is short-term health insurance worth it in Texas?

Short-term health insurance in Texas is worth it when three conditions line up. You are reasonably healthy, your coverage gap is finite, and you have weighed the trade-offs against ACA and COBRA. For chronic conditions, planned pregnancies, or long-term needs, short-term coverage is usually the wrong tool.

A short-term plan can be a real lifeline for the right applicant. Premiums of $90 to $200 per month, versus $700 per month under COBRA, can free up cash during a transition. Coverage starts the next day, with no waiting period. And for healthy young adults, the exclusions rarely apply.

But the plans are not “real” insurance under the ACA. They can decline applicants. They can deny claims tied to pre-existing conditions. And they can leave members exposed to large bills if the fine print hides a benefit cap. The right answer depends entirely on the applicant’s health, the gap length, and the alternative options available.

The cleanest way to answer “is it worth it for me” is a short conversation with a licensed Texas broker who can put short-term, ACA, COBRA, and employer coverage side by side.

This is a personal decision based on health, income, and life circumstances. There is no one-size answer.

Closing thoughts

Short-term health insurance in Texas has changed significantly since August 2025. Plans can now be structured for up to 3 years in most cases, premiums remain a fraction of ACA Bronze, and carriers like Blue Cross Blue Shield of Texas, UnitedHealthcare, Aetna, Cigna, and Humana all have a presence in this market at various points.

The trade-offs around pre-existing conditions, essential benefits, and post-claims underwriting remain unchanged.

For most Texans facing a coverage gap, the smart move is a no-pressure conversation with a licensed broker who can compare every option on the table.

Three things to do next:

- Write down the exact length of your coverage gap and your basic health profile.

- List anything you cannot afford to lose, such as a specific doctor, pharmacy, or planned procedure.

- Schedule a quick call with a licensed Texas broker to compare short-term, ACA, and COBRA options side-by-side.

A short conversation can clarify whether short-term health insurance is the right move for your situation, or whether a different path serves you better.