For Texas residents seeking private health insurance for their families, it is important to understand the key factors in selecting an appropriate plan. Texas family health insurance plans are purchased either directly from insurance companies or through a Texas-licensed agent.

When evaluating your options, consider your family’s healthcare needs, budget constraints, preferred healthcare providers, and the frequency with which your family typically utilizes medical services.

By carefully comparing monthly premiums, deductibles, out-of-pocket maximums, and network rules, you can identify the plan that best aligns with your family’s requirements.

You know, picking a family plan in Texas can feel confusing. Texas family health insurance plans vary in price, deductibles, and networks.

These are buy-your-own private plans, and you can easily get help through an agent if needed. You do not need to be an expert; support is available for every step.

Many people choose solely based on the monthly premium, but you can feel more secure by comparing premiums, deductibles, and out-of-pocket maxes in this guide.

It’s also important to consider less obvious cost factors, such as narrow networks or tiered prescription plans, which can significantly affect your overall costs.

By looking beyond surface numbers, you can ensure your doctors and hospitals are covered and gain peace of mind.

- Pick a monthly budget.

- List your doctors and hospitals.

- Compare deductible and out-of-pocket max.

- Choose the right plan type for your family.

If rushing, pick a budget, list doctors/hospitals, check in-network status, and get 2–3 quotes.

- List your doctors + hospitals.

- Check in-network before applying.

- Compare deductible + out-of-pocket max

- Get 2–3 quotes and choose

Next, let’s tackle a common question: what is the best health insurance plan for a family in Texas?

The best Texas family plan is the one you can afford each month and actually use, with your doctors in-network and total costs matching your risk level.

If you are comparing the best family health insurance plans in Texas, use this quick framework:

- Budget: a premium you can pay every month.

- Doctors: your key doctors and hospitals are in the network.

- Use: how often you expect visits, tests, and prescriptions.

- Risk: deductible and out-of-pocket max you could handle in a bad year.

Shortlist two or three options. Compare “best case” and “worst case.”

The “best” plan depends on your family’s health needs and finances.

Now that you know what makes a plan ‘best,’ consider where to buy private family health insurance in Texas.

You can buy private Texas family plans either directly from one company or through a licensed agent who helps you compare options across more than one company.

Two common paths (a common way families compare family health insurance providers in Texas

- Carrier-direct: you shop with one company and choose from that one menu.

- Agent/broker-assisted: You share your needs once and compare multiple options.

Direct shopping can work if you already know what you want. Agent support can help with network checks and comparisons.

Plan options depend on your ZIP code and family details.

Understanding where to buy, it’s also important to ask: Can you enroll in a private Texas family plan at any time of year?

Sometimes yes, but it depends on the product and the insurer’s rules. Many private plans use set enrollment windows or approval steps before coverage starts.

Private plans can vary widely by product. Some have fixed enrollment periods. Some ask health questions. Some services may have waiting periods.

The safest approach is to confirm timing before you cancel current coverage.

Timing checklist:

Confirm the earliest start date.

Timing impacts your first bill and your first month of access.

How to check:

- Ask if this product has an enrollment window.

- Ask if health questions/underwriting apply.

- Ask for the earliest effective date for your application.

- Ask about any waiting periods.

Do not cancel your current coverage until you have confirmed your new start date. This ensures a smooth transition and continuous protection for your family.

Enrollment rules vary by insurer and product, so confirm eligibility before you apply.

Cost is a key factor for most families, so how much does family health insurance cost per month in Texas?

Monthly cost depends on age, ZIP code, plan type, and cost-sharing. A lower premium often comes with a higher deductible and higher out-of-pocket risk.

You can compare plan designs for family health insurance plans in Texas, then pull quotes.

- Lower-premium plans may mean higher deductibles and out-of-pocket maxes.

- Higher premium plans may mean a lower deductible.

Example only. Not a quote. Not based on a specific plan.

| Scenario | Premium | Deductible | Out-of-pocket max |

| Lower premium / higher deductible | $400 | $8,000 | $16,000 |

| Higher premium / lower deductible | $750 | $2,500 | $9,000 |

Compare two or three quotes using your exact ages and ZIP code.

Checklist:

- Confirm the family deductible and out-of-pocket max (not just one person).

- Check copay and coinsurance for common services.

- Confirm the exact network name.

- Save the benefits summary you used to decide.

Only a real quote can show your exact monthly cost.

Different plan types offer varying experiences. Is an HMO or PPO better for families in Texas?

An HMO may cost less but can limit you to a smaller network. A PPO may cost more, but it may give more flexibility with doctors and specialists.

Plan type can shape your day-to-day experience.

- HMO: often lower premiums, but a tighter network and referral rules.

- PPO: often higher premiums, but more flexibility for doctors and specialists

- EPO: often in-network only except emergencies.

If you have “must-keep” doctors, start by confirming the network. Then choose the plan type that matches your budget and flexibility needs.

Plan rules and networks vary by company and location.

After the plan type, you’ll want to examine deductibles. What deductible is considered ‘good’ for a Texas family plan?

A “good” deductible is one you could pay out of savings if needed without causing major stress. It should match your budget and your comfort with risk.

Use a simple rule:

- If you have little savings, a lower deductible plan may feel safer.

- If you have a bigger cushion, a higher deductible plan may lower the premium. Always check the out-of-pocket max too. Example only. Not a quote. Not based on a specific plan.

- A deductible far above your savings can feel stressful. If you use a worksheet, keep it simple and use it for every plan you compare.

“Good” depends on your budget and health needs.

Plan costs also depend on how copays and coinsurance work. How do these apply to family plans?

A copay is a set fee for a visit or medicine. Coinsurance is a percentage you may pay after the deductible until you hit the out-of-pocket max.

These terms drive real-life costs.

- Copay: a set amount, like $40 per visit.

- Coinsurance: a percentage of allowed costs, like 20% after the deductible.

Copays matter more when your family uses care often, like kids’ visits and prescriptions. Coinsurance matters more for bigger bills, like imaging or hospital care.

Always confirm costs in the plan’s benefit summary.

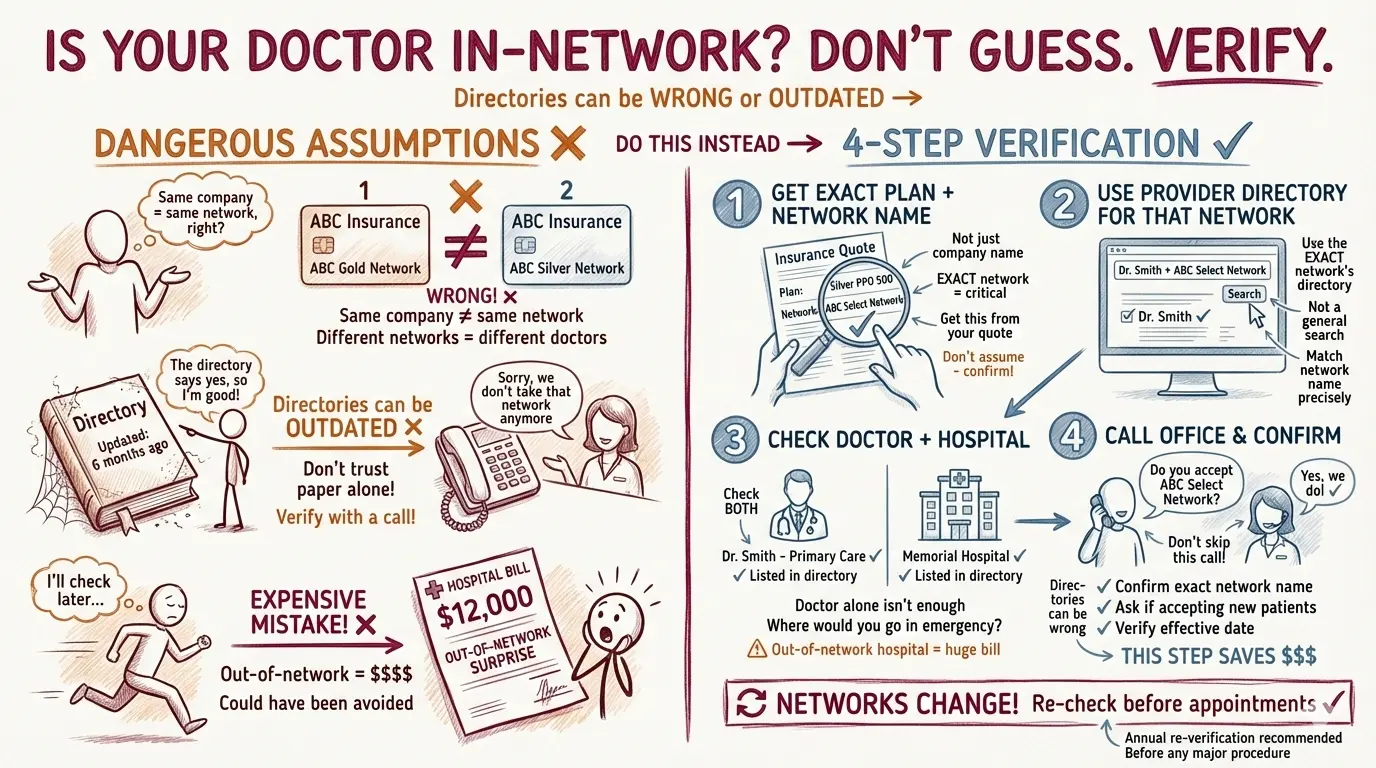

Before picking a plan, ensure your doctors are covered. How do you check if your doctor is in-network in Texas?

Use the provider search for the exact network, then call the doctor’s office to double-check before you apply, because directories can be wrong or outdated.

Do not guess on networks. “Same company” can still mean different networks.

Steps:

- Get the exact plan and network name from the quote.

- Use the provider directory for that network.

- Check the doctor and the hospital you would use.

- Call the office and confirm they take that exact network.

Networks can change, so re-check before appointments.

Families planning for maternity should also review this: Do Texas family plans cover maternity and newborn care?

Many family plans include maternity and newborn care, but what you pay depends on the plan and network, so you should verify OB/GYN and hospital details before you apply.

Maternity costs can be high, so small plan differences matter.

Confirm these items early:

- OB/GYN is in-network.

- The hospital is in-network.

- Prenatal visits: copay, deductible, or coinsurance?

- Delivery and inpatient stay cost-sharing.

If you are planning a baby soon, confirm timing and start dates.

Coverage and costs vary by insurer and plan design.

Children’s care matters too. Do family plans cover children’s dental and vision in Texas?

Some plans include children’s dental and vision coverage, while others require add-on coverage.

It depends on the plan, so check the benefits before you apply.

Do not assume kids’ dental and vision are included on private plans.

Check:

- Pediatric dental: included vs add-on.

- Vision exams: copay and frequency.

- Orthodontics: often limited.

Example only. Not a quote. Not based on a specific plan.

| Benefit | Included? | Add-on? |

| Kids dental cleanings | Sometimes | Sometimes |

| Kids vision exam | Sometimes | Sometimes |

| Braces | Rare | Sometimes |

If these benefits matter, include them in your quote request so you can compare them across plans.

Dental and vision benefits vary widely by plan.

Conclusion

Texas family health insurance plans are easier to navigate when you follow a simple order, and you can feel secure knowing there are clear steps to guide you.

Start with your monthly budget. Then confirm doctors and hospitals. After that, compare the deductible and out-of-pocket max to understand the worst-case risk.

Choose a plan type based on cost and flexibility. Pull two or three quotes and verify details before you switch.